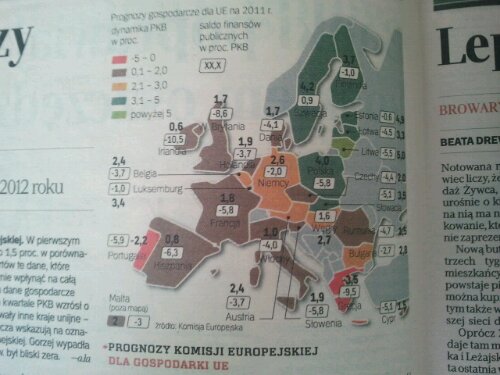

I think I’ll let the map speak for itself. It was the main story in the weekend edition of Rzeczpospolita newspaper.

I think I’ll let the map speak for itself. It was the main story in the weekend edition of Rzeczpospolita newspaper.

For businesses which have never been audited but which are growing up quickly to meet the audit thresholds in a year or two, you may wish to consider having your first audit done while it is still voluntary to do so, and the results, if less positive than expected, can at least be kept private.

Once your business has exceeded the audit thresholds (very typically in Europe this means for a private company about 50 employees, 5 million Euros turnover and 2.5 million Euros of gross assets, and it means 2 out of those three conditions – we just stated actually the Polish ones verbatim, (with the proviso that they also state a set PLN amount to avoid subjectivity for businesses that are on the cusp), but most countries are not far off that – even the Czech Republic which really needs much smaller thresholds)

Clearly this doesn’t apply at all to public limited companies, ie. the “S.A.”, “a.s.”, UK plc or German AG style companies which must be audited regardless of size – in some jurisdictions even if they are dormant – but for private limited liability companies most jurisdictions have size criteria like the ones just given – for Slovakia about 60% of the sizes given, so please note that this is divergent from the Czech ones, which are far too high for that country and result in proportionally fewer audits, which is a bad thing for corporate governance in that country.

While you are under the limits audit is voluntary. And you can have an unofficial audit whereby the audit comes and does for you all the normal work he would do if officially appointed, but it is only pro-forma. “Pro-forma” is Latin for something like the idea of “as if” so the auditor will work and report as if they had been properly appointed, but it is really a dry run for you. You do not appoint them as statutory auditors in the minuted general meeting, you do not have to file the report as the audit was voluntary, and you get all the benefit of the audit without the risk, and on top of all of that, I can get you these pro-forma audits for only 75% of the cost of a statutory audit, because the Firms we associate with want to promote good voluntary governance practice in the economy.

If you wait for your first audit until it is an obligatory one because you’ve outgrown the size criteria – and as we come out of the recession that will happen to some of you next year hopefully sooner than you dare hope for now – then if the auditor finds something wrong then the report of the auditor could be “modified” – I’ll do a separate article on what sorts of “modifications” exist and what they mean in accountancy speak, but it’s not good if you get one.

It will not help if you need a loan, and it will probably trigger a lot of interest on the part of the tax inspector. But you’ll have to publish it anyway, if there isn’t time to do the remedial work a good auditor should outline to you in time for your statutory deadline.

Now auditors get cajoled, encouraged in a friendly way or even outright threatened by desparate managers and owners to overlook things or change to an opinion that doesn’t match the facts, and there is nothing that can be done in those circumstances. Auditors are not generally anywhere near as afraid of their client as they are of their regulator, but more than that we are educated throughout our professional lives to be independent in our outlook, and so the only way to get out of some modified opinions is to do the remedial work the auditor recommends or make the adjustments that they recommend.

There’s no point in changing to another auditor you think will be more pliable – they must write to the old auditor and ask if there are any reasons why they cannot act. The best thing to do, if you are not sure how well your company will stand up to an audit is to have your first one a year or so before you need to. Then if the audit shows up a lot to be desired, you have a whole year to put it right and nobody will ever know because auditors are bound by confidentiality – it isn’t us who even publish our reports, it’s the responsibility of the client. The report is given to its addressee, which is always the shareholder, and some other corporate governance boards if they are in existence.

So it’s well worth thinking about, especially if your business has been growing fast and maybe has outgrown its systems.

Let us know if we can help.

You must be logged in to post a comment.