Why effective governance, auditing, and oversight depend on clarity, restraint, and role discipline

Good governance is often misunderstood. Many organisations behave as if oversight must be loud, dramatic, or ceremonially complex to be effective. But governance is not theatre. It is not a performance. It is a discipline rooted in clarity, proportionality, and the quiet confidence that comes from doing the right things consistently.

This article explores why governance fails when it becomes performative, drawing on classic cautionary tales, real‑world audit practice, and the recurring problem of Supervisory Boards drifting into executive territory. It concludes with a reminder from the “wise old owl” that the best oversight is often the quietest.

Governance and the Danger of Performative Oversight

Matilda and the problem of false alarms in governance

Hilaire Belloc’s Matilda is a perfect metaphor for governance gone wrong. Matilda repeatedly raised false alarms for the pleasure of the attention they brought. When the real fire came, nobody listened. She had exhausted the system’s capacity to take her seriously.

Many organisations fall into the same trap. They escalate everything. They dramatise routine matters. They mistake procedural fuss for foresight. And when a genuine governance risk finally emerges, the organisation is deafened by its own theatrics.

Key governance lesson: Oversight loses its power when everything is treated as urgent.

Edward Lear and the softer side of governance nonsense

Edward Lear’s nonsense characters offer a gentler warning. Their misadventures arise not from malice but from distraction, whimsy, or a love of spectacle. They are charming — but they are not models of governance.

Governance takeaway: Nonsense has its place, but not in the boardroom.

Audit Governance: When Emphasis of Matter Becomes a Song and Dance

The proper role of the Emphasis of Matter paragraph

The Emphasis of Matter (EoM) paragraph is a legitimate tool in the auditor’s report. It is used when:

- the auditor’s opinion is unmodified,

- management has already made full disclosure, and

- the auditor judges the matter so fundamental that it merits highlighting.

Used correctly, it enhances clarity.

The problem: overuse of Emphasis of Matter paragraphs

Some auditors use EoMs as if they were Matilda shouting “Fire!” — emphasising matters already perfectly disclosed, simply to appear diligent. This is governance by performance, not governance by principle.

Worse still, some auditors are tempted to disclose information in the EoM that management has not disclosed. This is a cardinal error. If the auditor feels compelled to introduce new information, the correct response is a modified opinion, not a theatrical EoM.

When Emphasis of Matter is appropriate

There are legitimate cases — for example, in publicly listed companies where a disclosure is technically complete but placed where a reasonable reader might not expect it. In such cases, an EoM enhances transparency.

But it should be the exception, not the rule.

Supervisory Boards and the Governance Failure of Role Confusion

When overseers drift into executive management

A second common governance failure occurs when Supervisory Board members begin to act like executives. They:

- rewrite management’s plans,

- involve themselves in operational decisions,

- direct staff,

- or behave as if they are auditioning for an executive role.

This is not oversight. It is role confusion. It comes from human nature and is related to the mission creep we see in national governments and state sectors using regulators and regulations to reduce the remit of privatye businesses. Oversight boards in the private sector need to know that the temptation is there in human nature, but they need to know better. Let the execs do their job, give them duue encouragement, help them think, be a sparring partner when required, and know when to butt out when not.

The revolving‑door problem

In some organisations, careers shuttle between executive and non‑executive roles. This creates:

- blurred accountability,

- conflicts of interest,

- weakened independence,

- and a governance structure that looks busy but functions poorly.

An overseer who expects to become an operator tomorrow cannot hold today’s operators to account.

A historical contrast: overseers in the early church

The early church used the term episkopos — overseer — for individuals who were spiritually mature but still ordinary members of the community. Their authority came from example, not executive power.

Modern corporate governance is different, but the contrast is instructive:

- Church oversight is pastoral.

- State oversight is constitutional.

- Business oversight is fiduciary.

These are three strands of a threefold cord not quickly broken — but only when each strand keeps its integrity.

Governance takeaway

Oversight is not a rehearsal for executive office. It is not shadow‑management. It is a separate vocation requiring distance, independence, and clarity.

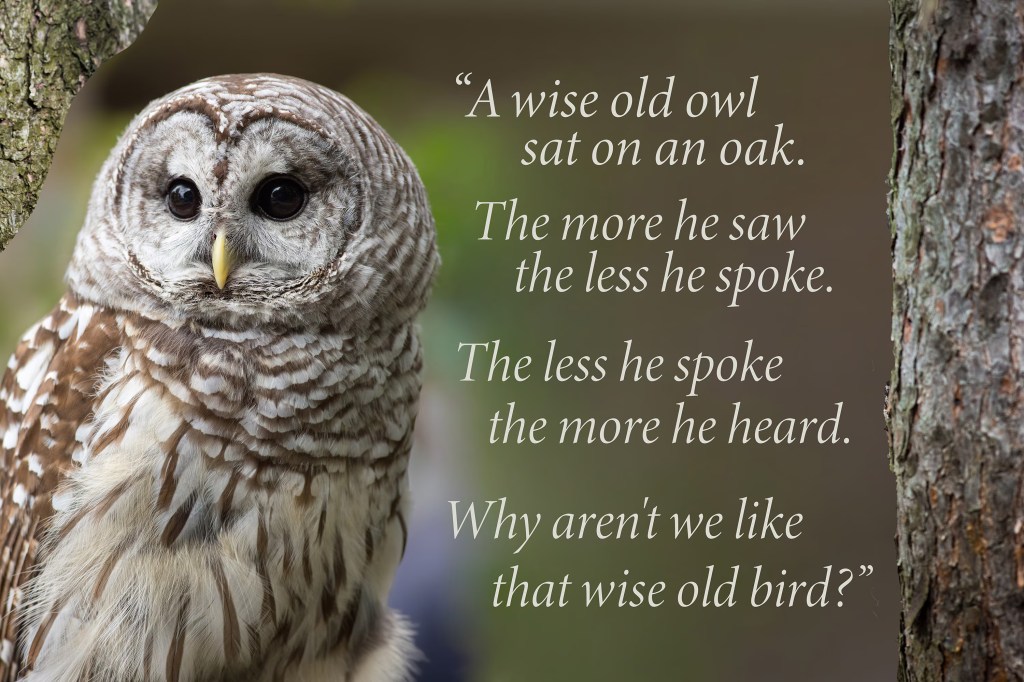

Coda: The Wise Old Owl and the Power of Quiet Oversight

The old nursery verse about the wise old owl, usually attributed to Edward Hersey Richards, captures the heart of effective governance:

The more he saw, the less he spoke; The less he spoke, the more he heard.

It is a child’s rhyme, but it contains a governance truth many adults never learn.

Oversight — whether by non‑executive directors, auditors, regulators, or Supervisory Boards — is most effective when it is:

- observant rather than intrusive,

- attentive rather than theatrical,

- measured rather than noisy.

If overseers make a fuss over everything, they become like Matilda: ignored when it matters. If they try to do management’s job, they lose the independence that gives oversight its value. If they speak too often or too loudly, they find that when they finally need to be heard, their voice no longer carries.

Good governance listens more than it lectures. It intervenes only when intervention is truly needed. And when it speaks — really speaks — people listen.

And what we can say about corporate governance is no less true when we speak about the government of nations.

This Latin songstress could be described as something like Shakira meets Rita Ora meets Julio Iglesias. Could be described, that is, if she existed as an actual pop star rather than an accounting mnemonic.

This Latin songstress could be described as something like Shakira meets Rita Ora meets Julio Iglesias. Could be described, that is, if she existed as an actual pop star rather than an accounting mnemonic. Accountancy is the language of business. Not always the language of macro-economics which is why that can go haywire, but of business it is. It is the way in which we keep things making sense and not having assets and liabilities which correspond to nothing but someone’s desire that they should be there, with no basis in fact.

Accountancy is the language of business. Not always the language of macro-economics which is why that can go haywire, but of business it is. It is the way in which we keep things making sense and not having assets and liabilities which correspond to nothing but someone’s desire that they should be there, with no basis in fact.

You must be logged in to post a comment.