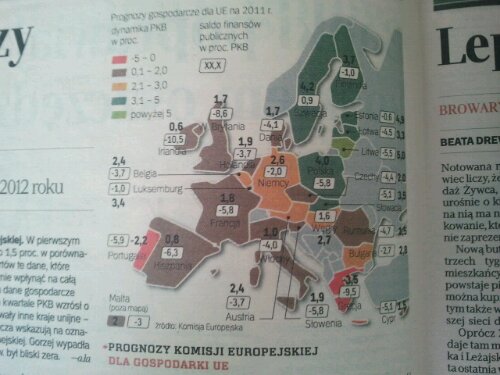

I think I’ll let the map speak for itself. It was the main story in the weekend edition of Rzeczpospolita newspaper.

I think I’ll let the map speak for itself. It was the main story in the weekend edition of Rzeczpospolita newspaper.

David James et Lucia Rablova de Baker Tilly Tchequie ont ecrit cette article avec Mme Valerie Malnoy de Baker Tilly France, qui est apparu dans l’edition de decembre 2010. Nous esperons que ce contient sera interessant pour nos lecteurs francophones.

Les firmes associes de Baker Tilly sont a meme de servir des clients francophones en francais dans le plupart de la region de l’Europe de l’Est.

2010-12-08~1527@L_ENTREPRISE Rép Tchèque

Et ici vous trouverez le site de Baker Tilly Republique Tcheque en francais.

You may have received e-mail (especially from Chinese and Hong Kong companies relating to .cn domains bearing your name if you didn’t register in China, but now more commonly in East Europe also) which says that if you use these people’s services they can prevent your name’s domain in that country from getting blocked.

Now this email gets sent out all over the world to addresses harvested from the internet page and chats and from usenet fora by robots, and of course the people behind the email cannot really afford to block every single domain that they are fishing for. The one sure fire way of making sure that they do block your domain is if you respond to them, whether with threats or with asking for the help, even in terms of “what it would cost”. I suggest you only do this if you don’t want the domain really and have no intention of buying it, as if you are lucky it will lead the scammers into real cash outlay which they’ll never see any return on. I highly encourage that! Maybe some of these pests will stop it if they see that enough internet users are wise to them and don’t mind leading them up a garden path…

You can always search here on EuroDNS (in the interests of transparency that affiliate link earns 10% of anything you buy after you go there, but it shouldn’t cost you more and it’s the service I use myself) and see what the status is of all of your possible combinations of your name and the country endings or generic endings, as well as check the Whois status of all these countries, both Europe and Asia, all in one place. You will probably find that nobody has blocked your domain at all, and if you are interested in owning the domain you can block it there and then. They are ethical and I never had a problem with them that the owner didn’t solve within a week. If they are not contactable one day you can usually get them the next day. Continue reading “Domain names scam – what to do if affected”

For businesses which have never been audited but which are growing up quickly to meet the audit thresholds in a year or two, you may wish to consider having your first audit done while it is still voluntary to do so, and the results, if less positive than expected, can at least be kept private.

Once your business has exceeded the audit thresholds (very typically in Europe this means for a private company about 50 employees, 5 million Euros turnover and 2.5 million Euros of gross assets, and it means 2 out of those three conditions – we just stated actually the Polish ones verbatim, (with the proviso that they also state a set PLN amount to avoid subjectivity for businesses that are on the cusp), but most countries are not far off that – even the Czech Republic which really needs much smaller thresholds)

Clearly this doesn’t apply at all to public limited companies, ie. the “S.A.”, “a.s.”, UK plc or German AG style companies which must be audited regardless of size – in some jurisdictions even if they are dormant – but for private limited liability companies most jurisdictions have size criteria like the ones just given – for Slovakia about 60% of the sizes given, so please note that this is divergent from the Czech ones, which are far too high for that country and result in proportionally fewer audits, which is a bad thing for corporate governance in that country.

While you are under the limits audit is voluntary. And you can have an unofficial audit whereby the audit comes and does for you all the normal work he would do if officially appointed, but it is only pro-forma. “Pro-forma” is Latin for something like the idea of “as if” so the auditor will work and report as if they had been properly appointed, but it is really a dry run for you. You do not appoint them as statutory auditors in the minuted general meeting, you do not have to file the report as the audit was voluntary, and you get all the benefit of the audit without the risk, and on top of all of that, I can get you these pro-forma audits for only 75% of the cost of a statutory audit, because the Firms we associate with want to promote good voluntary governance practice in the economy.

If you wait for your first audit until it is an obligatory one because you’ve outgrown the size criteria – and as we come out of the recession that will happen to some of you next year hopefully sooner than you dare hope for now – then if the auditor finds something wrong then the report of the auditor could be “modified” – I’ll do a separate article on what sorts of “modifications” exist and what they mean in accountancy speak, but it’s not good if you get one.

It will not help if you need a loan, and it will probably trigger a lot of interest on the part of the tax inspector. But you’ll have to publish it anyway, if there isn’t time to do the remedial work a good auditor should outline to you in time for your statutory deadline.

Now auditors get cajoled, encouraged in a friendly way or even outright threatened by desparate managers and owners to overlook things or change to an opinion that doesn’t match the facts, and there is nothing that can be done in those circumstances. Auditors are not generally anywhere near as afraid of their client as they are of their regulator, but more than that we are educated throughout our professional lives to be independent in our outlook, and so the only way to get out of some modified opinions is to do the remedial work the auditor recommends or make the adjustments that they recommend.

There’s no point in changing to another auditor you think will be more pliable – they must write to the old auditor and ask if there are any reasons why they cannot act. The best thing to do, if you are not sure how well your company will stand up to an audit is to have your first one a year or so before you need to. Then if the audit shows up a lot to be desired, you have a whole year to put it right and nobody will ever know because auditors are bound by confidentiality – it isn’t us who even publish our reports, it’s the responsibility of the client. The report is given to its addressee, which is always the shareholder, and some other corporate governance boards if they are in existence.

So it’s well worth thinking about, especially if your business has been growing fast and maybe has outgrown its systems.

Let us know if we can help.

The main considerations are grouped under headings

LEGAL

• The scope of business of the branch may not be broader than the scope of business of the foreign entity.

• The branch must publish the financial statements of the foreign company in the registry of documents kept by the Commercial Register, which effectively means getting the whole report of the company the branch is part of and translating it into Czech, and publicising it even if the accounts were not liable to be made public in the jurisdiction of the Company.

ACCOUNTING

• In general the same statutory obligations apply for both branch and legal entity from accounting and financial reporting point of view, i.e. every corporate entity doing business in Czech Republic must keep the books in Czech language and must file the financial statements to the Commercial Register.

• The only difference we can see is that the statutory financial statements of branch are to be incorporated into the statutory accounts of the founder whereas in case of legal entity financial statements stands alone and the financial asset (i.e. investment in the subsidiary) is to be shown in the accounts of the parent company. Branches do not really have separate equity, as they are not legal persons, but in order for the balance sheet to balance the capital employed needs to be shown as if they were, on a pro-forma basis. Likewise purchases of goods by the branch from the company it is part of is legal nonsense, as there is no tranfer of ownership to a branch, but still in order to give a picture of the performance of the branch as well as to be above board with regard to international transfer pricing, again branch accounts should be done with these intra-company “sales” and “purchases” included as pro forma. Remember that the branch has its own tax life in the country where it is.

AUDIT

• The same statutory obligations apply for both branch and legal entity to have its accounts audited.

• The general rules are as follows:

1) joint stock companies One of the following criterions is met for two consecutive accounting periods: a) gross assets of 40.000K CZK b) revenues of 80.000K CZK c) average number of employees over 50.

2) other legal entities (limited liability companies, branches, etc.) Two of three above criterions are met for two consecutive accounting periods.

TAX

• From the Czech corporate taxation point of view the branch must register for corporate income tax only if having taxable income in the Czech Republic through a permanent establishment, the legal entity must register in any case.

• In case of the branch the income and costs need to be allocated to branch activities, however keeping in mind transfer pricing and substance-over-form principle that are applicable under both structures, i.e. under both branch and legal entity constructs.

• Profits/losses will be included in profits of the founder of the branch taking into consideration double taxation reliefs.

• From the VAT perspective in case of the branch the VAT payer is actually the headquarter that has Czech VAT registration while in case of the legal entity it is actually the entity itself being Czech VAT payer.

• Profit repatriation in the case of the legal entity must be taken into account, however, if the parent company being an EU entity with more than 10% shareholding for more than 12 months dividend payments are tax exempt.

| Subsidiary | Branch | |

| Tax registration | obligatory | Only if taxable income from sources in the Czech Republic |

| Tax at operational level | 19% CIT | 19% CIT |

| Tax at parent/headquarter level in respect of subsidiary’/branch’s profits | Participation exemption or tax credit (in cases of dividend distribution) | Tax rate of the headquarter (note: double taxation relief ® participation exemption or tax credit) |

| Withholding tax (dividend, interest, royalties) | Often (note: EC Directives and tax treaties) | Rarely |

| Loss settlement with foreign parent company/headquarter | In principle no | Yes (unless exempt under headquarters’ domestic tax law) |

| Liability debt (claims) at operational level | Local operating company (=subsidiary) | Headquarter |

The above was based on the amiable co-operation of TGC Corporate Lawyers and Baker Tilly sro in Prague and Brno.

If you have HR matters to look after in the Czech Republic, you probably know how tricky it can be. Here is a sample of Contract Administration Czech Republic’s excellent HR newsletter, which is a very readable and relevant update of the ever-changing world of Czech labour law and payroll tax and insurance issues.

Contract Administration Czech Republic’s June HR Newsletter

This is set fair to become one of the most popular pdf-casts in the Czech business universe. To get a regular copy, contact Contract Administration via their website .

Their highly reputed personnel administration service is available from their offices in Prague, Bratislava, Warsaw and Wroclaw.

You must be logged in to post a comment.